Introduction

In the previous post I shared my journey of getting SageMath installed in Windows and writing my first unit tests.

In this blog we will build our own symbolic Ito calculus layer on top of SageMath and use it to derive the Black-Scholes partial differential equation (PDE) directly from the stochastic differential equation (SDE) of the underlying asset.

Rather than manipulating the formulas by hand, we let the SageMath algebra engine apply our own custom-built Ito lemma, symbolically and verify the structure of the PDE step-by-step.

Setting Up Geometric Brownian Motion in Python

We begin with the standard geometric Brownian motion model for the underlying asset price:

where

with variables already declared as SageMath var types:

var types, we first declare the variables that we will use.Now, let’s assume the derivative price is a smooth function

Our goal is to compute

Spoiler alert, it will be as simple as executing the following in python:

with console output:

Let’s get into it.

Encoding the Ito Algebra

Since SageMath does not natively implement stochastic calculus rules, such as

and multiplication rules enforce:

and we must allow symbolic quadratic variation to emerge automatically.

from dataclasses import dataclassfrom typing import Dictfrom sage.all import SR, var, diff # type: ignoredataclass(frozen=True)class Ito: a: object b: object c: Dict[int, object] def __add__(self, other): if not isinstance(other, Ito): other = Ito.scalar(other) c_new = dict(self.c) for i, ci in other.c.items(): c_new[i] = c_new.get(i, 0) + ci if c_new[i] == 0: del c_new[i] return Ito(self.a + other.a, self.b + other.b, c_new) def __radd__(self, other): # allows: 0 + Ito(...) and scalar + Ito(...) return self.__add__(other) def __neg__(self): return Ito(-self.a, -self.b, {i: -ci for i, ci in self.c.items()}) def __sub__(self, other): return self.__add__(-other) def __rsub__(self, other): return Ito.scalar(other).__sub__(self) staticmethod def scalar(x): return Ito(SR(x), 0, {}) staticmethod def dt(coeff=1): return Ito(0, SR(coeff), {}) staticmethod def dW(i, coeff=1): return Ito(0, 0, {i: SR(coeff)}) def __mul__(self, other): if not isinstance(other, Ito): other = Ito.scalar(other) a1, b1, c1 = self.a, self.b, self.c a2, b2, c2 = other.a, other.b, other.c a = a1 * a2 c = {} for i in set(c1) | set(c2): ci = a1 * c2.get(i, 0) + a2 * c1.get(i, 0) if ci != 0: c[i] = ci b = a1 * b2 + a2 * b1 for i in set(c1) & set(c2): b += c1[i] * c2[i] return Ito(a, b, c) def __repr__(self): parts = [str(self.a)] if self.b != 0: parts.append(f"{self.b}*dt") for i in self.c: parts.append(f"{self.c[i]}*dW{i}") return " + ".join(parts)

The core idea of this class is simple: it represents stochastic differentials as truncated objects of the form

where

is a scalar,

is the coefficient of

, and

are the coefficients of the Brownian increments.

You can see that we have explicitly encoded the Ito multiplication rules, which is where stochastic calculus differs fundamentally from classical calculus.

The Structure of the Ito Class

The Ito object stores the aforementioned three components:

So for example,

dX = Ito.dt(mu * S) + Ito.dW(1, sigma * S)

would represent

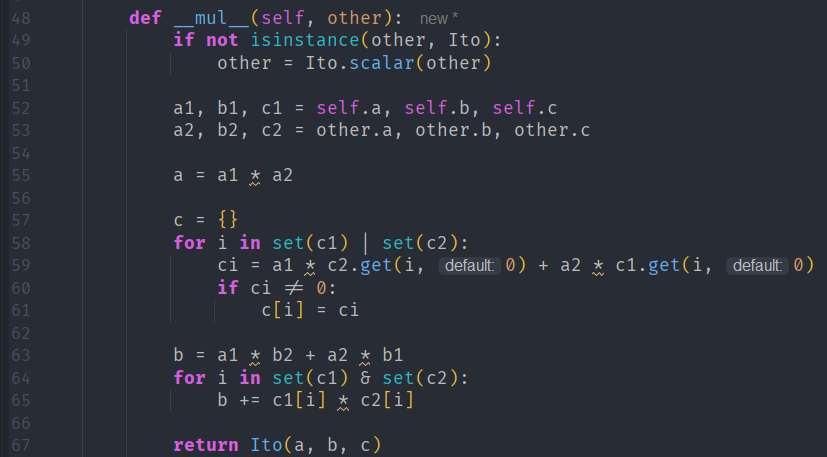

Multiplication

The multiplication method __mul__ is important, because it obeys the Ito calculus multiplication rules. This means that when we multiply, say

the class method will drop all

The quadratic variation term is handled explicitly,

This line encodes

Everything else is standard algebra.

Why Does This Matter?

Because once multiplication is handled, quadratic variation should emerge automatically. So, for example,

dX = mu dt + sigma dWdX2 = dX * dX

yields:

without having to write a single special case.

The Ito Lemma Layer

With the algebra defined, we implement the (1-dimensional) Ito lemma as a function. For the 1D diffusion

where subscripts represent partial derivatives.

Since our Ito algebra already computes

This produces an Ito object containing all the data needed to represent

Some Extensions

Multi-factor Extension

For scalar

Ito’s lemma becomes:

Our implementation allows this, for example, this line

corresponds to computing

Generator Extraction

We also implement the infinitesimal generator:

= f_t + \mu f_{x} + \displaystyle\frac{1}{2}\sigma^2 f_{xx}](https://s0.wp.com/latex.php?latex=%5Cmathcal%7BL%7D%5Bf%5D%28t%2Cx%29+%3D+f_t+%2B+%5Cmu+f_%7Bx%7D+%2B+%5Cdisplaystyle%5Cfrac%7B1%7D%7B2%7D%5Csigma%5E2+f_%7Bxx%7D&bg=%23ffffff&fg=%23111111&s=0&c=20201002)

which is the drift term of

Matching the drift term against

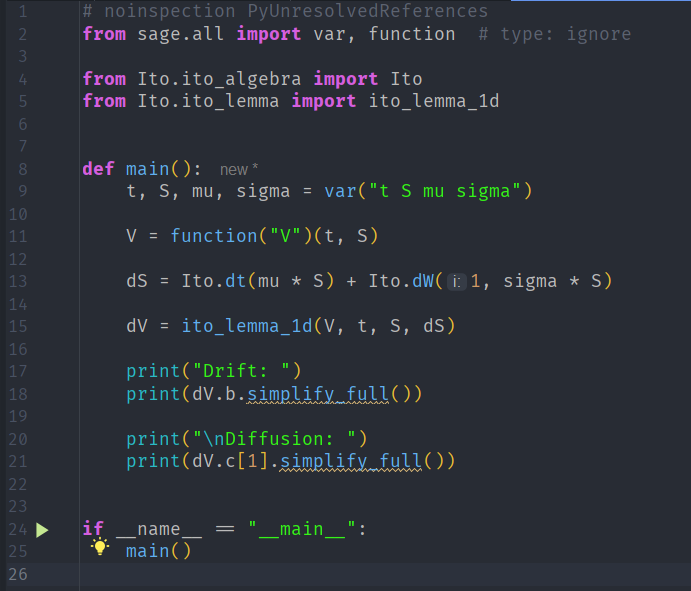

Applying Ito’s Lemma Symbolically

Using our custom ito_lemma_1d function, we compute

with the following command

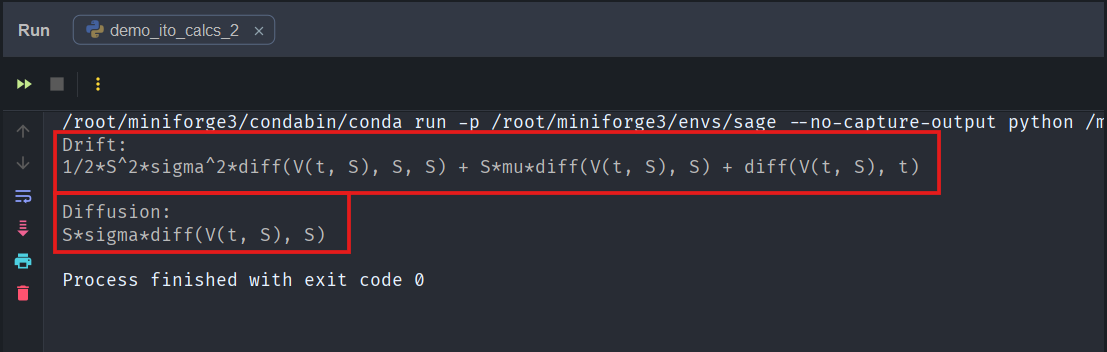

and the symbolic engine produces the drift term,

and diffusion term,

Conclusion

Our design separates algebra from calculus:

ito_algebra.pyencodes the stochastic multiplication rules,ito_lemma.pyencodes the calculus layer,SageMathhandles the symbolic differentiation

and the Black-Scholes PDE drops out automatically!

References

Appendix

Ito_algebra.py

from dataclasses import dataclassfrom typing import Dictfrom sage.all import SR, var, diff # type: ignoredataclass(frozen=True)class Ito: a: object b: object c: Dict[int, object] def __add__(self, other): if not isinstance(other, Ito): other = Ito.scalar(other) c_new = dict(self.c) for i, ci in other.c.items(): c_new[i] = c_new.get(i, 0) + ci if c_new[i] == 0: del c_new[i] return Ito(self.a + other.a, self.b + other.b, c_new) def __radd__(self, other): # allows: 0 + Ito(...) and scalar + Ito(...) return self.__add__(other) def __neg__(self): return Ito(-self.a, -self.b, {i: -ci for i, ci in self.c.items()}) def __sub__(self, other): return self.__add__(-other) def __rsub__(self, other): return Ito.scalar(other).__sub__(self) staticmethod def scalar(x): return Ito(SR(x), 0, {}) staticmethod def dt(coeff=1): return Ito(0, SR(coeff), {}) staticmethod def dW(i, coeff=1): return Ito(0, 0, {i: SR(coeff)}) def __mul__(self, other): if not isinstance(other, Ito): other = Ito.scalar(other) a1, b1, c1 = self.a, self.b, self.c a2, b2, c2 = other.a, other.b, other.c a = a1 * a2 c = {} for i in set(c1) | set(c2): ci = a1 * c2.get(i, 0) + a2 * c1.get(i, 0) if ci != 0: c[i] = ci b = a1 * b2 + a2 * b1 for i in set(c1) & set(c2): b += c1[i] * c2[i] return Ito(a, b, c) def __repr__(self): parts = [str(self.a)] if self.b != 0: parts.append(f"{self.b}*dt") for i in self.c: parts.append(f"{self.c[i]}*dW{i}") return " + ".join(parts)

ito_lemma.py

from __future__ import annotationsfrom typing import Dict, Tuple# noinspection PyUnresolvedReferencesfrom sage.all import var, SR, diff # type: ignorefrom Ito.ito_algebra import Itodef _as_symbolic(x): """Coerce x into Sage's symbolic ring when possible.""" try: return SR(x) except Exception: return xdef _extract_mu_sigmas(dX: Ito) -> Tuple[object, Dict[int, object]]: """ Given dX = mu*dt + sum_i sigma_i*dW_i (Ito object), return (mu, sigmas_dict). We expect dX.a == 0 for a differential. If it's not, we don't hard-fail, but you should probably not be passing a nonzero scalar part as a "dX". """ mu = dX.b sigmas = dict(dX.c) return mu, sigmasdef ito_lemma_1d(f, t, x, dX: Ito, dw_index: int = 1) -> Ito: """ Itô's lemma for f(t, X_t) with 1D state X driven by ONE Brownian component dW_{dw_index}. Input: f : Sage expression in (t, x) t, x : Sage symbols dX : Ito object representing dX = mu*dt + sigma*dW_{dw_index} dw_index : which Brownian index to use as the 1D driver Output: df as Ito object: df = drift*dt + diffusion*dW_{dw_index} """ ft = diff(f, t) fx = diff(f, x) fxx = diff(fx, x) mu, sigmas = _extract_mu_sigmas(dX) sigma = sigmas.get(dw_index, 0) drift = ft + fx * mu + SR(1) / SR(2) * fxx * (sigma ** 2) diffusion = fx * sigma return Ito.dt(drift) + Ito.dW(dw_index, diffusion)def ito_lemma_scalar_state_multiW(f, t, x, dX: Ito) -> Ito: """ Itô's lemma for scalar state X driven by multiple independent Brownian motions: dX = mu*dt + sum_i sigma_i dW_i where dW_i dW_j = delta_ij dt. Then: df = f_t dt + f_x dX + 1/2 f_xx (sum_i sigma_i^2) dt = [f_t + f_x mu + 1/2 f_xx * sum_i sigma_i^2] dt + sum_i f_x sigma_i dW_i """ ft = diff(f, t) fx = diff(f, x) fxx = diff(fx, x) mu, sigmas = _extract_mu_sigmas(dX) sig_sq = sum((si ** 2) for si in sigmas.values()) drift = ft + fx * mu + SR(1) / SR(2) * fxx * sig_sq out = Ito.dt(drift) for i, si in sigmas.items(): out = out + Ito.dW(i, fx * si) return outdef generator_L_1d(f, t, x, mu, sigma): """ Infinitesimal generator for a 1D Itô diffusion: dX = mu(t,x) dt + sigma(t,x) dW L f = f_t + mu f_x + 1/2 sigma^2 f_xx Useful for Feynman–Kac sanity checks. """ ft = diff(f, t) fx = diff(f, x) fxx = diff(fx, x) return ft + mu * fx + SR(1) / SR(2) * (sigma ** 2) * fxx

test_ito_lemma.py

import unittest# noinspection PyUnresolvedReferencesfrom sage.all import var, SR, sin # type: ignorefrom Ito.ito_algebra import Itofrom Ito.ito_lemma import ito_lemma_1d, ito_lemma_scalar_state_multiW, generator_L_1ddef assert_sage_expr_zero(testcase: unittest.TestCase, expr, msg: str = ""): """ Robust "expr == 0" for Sage symbolic expressions. """ e = SR(expr).simplify_full() testcase.assertTrue(e == 0, msg or f"Expected 0, got {e}")def assert_sage_expr_equal(testcase: unittest.TestCase, lhs, rhs, msg: str = ""): """ Robust symbolic equality check: lhs == rhs. """ assert_sage_expr_zero(testcase, SR(lhs) - SR(rhs), msg or f"{lhs} != {rhs}")class TestItoLemma(unittest.TestCase): def test_ito_lemma_x_squared_1d(self): # f(x) = x^2, dX = mu dt + sigma dW t, x, mu, sigma = var("t x mu sigma") f = x**2 dX = Ito.dt(mu) + Ito.dW(1, sigma) df = ito_lemma_1d(f, t, x, dX, dw_index=1) # Expected: df = (2x*mu + sigma^2) dt + (2x*sigma) dW expected_drift = 2 * x * mu + sigma**2 expected_diff = 2 * x * sigma assert_sage_expr_equal(self, df.a, 0, "df should have no scalar term") assert_sage_expr_equal(self, df.b, expected_drift, "wrong drift for x^2") self.assertIn(1, df.c, "missing dW1 term") assert_sage_expr_equal(self, df.c[1], expected_diff, "wrong diffusion for x^2") def test_ito_lemma_constant_function_is_zero(self): t, x, mu, sigma = var("t x mu sigma") f = SR(7) # constant dX = Ito.dt(mu) + Ito.dW(1, sigma) df = ito_lemma_1d(f, t, x, dX, dw_index=1) assert_sage_expr_equal(self, df.a, 0) assert_sage_expr_equal(self, df.b, 0) self.assertEqual(df.c, {}) def test_ito_lemma_linear_function(self): # f(t,x) = a*x + b*t t, x, a, b, mu, sigma = var("t x a b mu sigma") f = a * x + b * t dX = Ito.dt(mu) + Ito.dW(1, sigma) df = ito_lemma_1d(f, t, x, dX) # f_t = b, f_x = a, f_xx = 0 expected_drift = b + a * mu expected_diff = a * sigma assert_sage_expr_equal(self, df.b, expected_drift) assert_sage_expr_equal(self, df.c[1], expected_diff) def test_ito_lemma_multiW_scalar_state(self): # Scalar X driven by 2 independent Brownian motions t, x, mu, s1, s2 = var("t x mu s1 s2") f = x**3 + t * x dX = Ito.dt(mu) + Ito.dW(1, s1) + Ito.dW(2, s2) df = ito_lemma_scalar_state_multiW(f, t, x, dX) # Compute expected manually: # f_t = x # f_x = 3x^2 + t # f_xx = 6x fx = 3 * x**2 + t ft = x fxx = 6 * x expected_drift = ft + fx * mu + SR(1) / SR(2) * fxx * (s1**2 + s2**2) expected_dW1 = fx * s1 expected_dW2 = fx * s2 assert_sage_expr_equal(self, df.a, 0) assert_sage_expr_equal(self, df.b, expected_drift) self.assertIn(1, df.c) self.assertIn(2, df.c) assert_sage_expr_equal(self, df.c[1], expected_dW1) assert_sage_expr_equal(self, df.c[2], expected_dW2) def test_generator_matches_drift_part_1d(self): # For 1D: drift from Ito lemma should equal Lf where L is generator, # for f(t,x) with dX = mu dt + sigma dW, excluding diffusion terms. t, x, mu, sigma = var("t x mu sigma") f = sin(x) + t**2 dX = Ito.dt(mu) + Ito.dW(1, sigma) df = ito_lemma_1d(f, t, x, dX) Lf = generator_L_1d(f, t, x, mu, sigma) assert_sage_expr_equal(self, df.b, Lf, "Ito drift should equal generator Lf") def test_ito_lemma_multiW_reduces_to_1d_when_one_factor(self): # multiW formula should match 1D formula if only one dW term exists t, x, mu, sigma = var("t x mu sigma") f = x**4 dX = Ito.dt(mu) + Ito.dW(1, sigma) df1 = ito_lemma_1d(f, t, x, dX) dfm = ito_lemma_scalar_state_multiW(f, t, x, dX) assert_sage_expr_equal(self, df1.b, dfm.b) self.assertEqual(set(df1.c.keys()), set(dfm.c.keys())) assert_sage_expr_equal(self, df1.c[1], dfm.c[1])if __name__ == "__main__": unittest.main()

demo_ito_calcs_1.py

# noinspection PyUnresolvedReferencesfrom sage.all import var, sin, exp, SRfrom Ito.ito_algebra import Ito # type: ignorefrom Ito.ito_lemma import ito_lemma_1d, ito_lemma_scalar_state_multiW, generator_L_1ddef show(label, ito_obj: Ito): print("\n" + label) print(" scalar a =", ito_obj.a) print(" dt b =", ito_obj.b) print(" dW c =", ito_obj.c)def main(): t, x, mu, sigma = var("t x mu sigma") # 1) Basic differential and quadratic variation dX = Ito.dt(mu) + Ito.dW(1, sigma) show("dX = mu dt + sigma dW1", dX) dX2 = dX * dX show("dX^2 (should be sigma^2 dt)", dX2)if __name__ == "__main__": main()

demo_ito_calcs.py

# noinspection PyUnresolvedReferencesfrom sage.all import var, function # type: ignorefrom Ito.ito_algebra import Itofrom Ito.ito_lemma import ito_lemma_1ddef main(): t, S, mu, sigma = var("t S mu sigma") V = function("V")(t, S) dS = Ito.dt(mu * S) + Ito.dW(1, sigma * S) dV = ito_lemma_1d(V, t, S, dS) print("Drift: ") print(dV.b.simplify_full()) print("\nDiffusion: ") print(dV.c[1].simplify_full())if __name__ == "__main__": main()